Mega Backdoor Roth 401(k): Instruction & Strategy

What is the Mega Backdoor Roth 401k?

The Mega Backdoor Roth 401(k) strategy represents one of the most powerful tools available to high-income earners seeking to optimize their retirement savings. By leveraging after-tax contributions and in-plan Roth conversions, this approach allows individuals to bypass Roth IRA income limits, contribute up to $70,000 annually to tax-advantaged retirement accounts, and secure tax-free growth and withdrawals in retirement.

- This strategy is only applicable for individuals who are currently or planning to maximize their employee contribution 401k savings up to the annual IRS limits: $23,500 in 2025 for those below age 50, $31,000 for those 50 and older. The Mega Backdoor Roth strategy allows employees to save above and beyond these regular annual limits.

This guide explores the mechanics, eligibility criteria, strategic benefits, and implementation considerations for what we consider an advanced financial planning strategy.

This guide should be used as educational material only and should be implemented in conjunction with a strategic financial planning strategy. Talk to your financial planner and/or tax professional before implementing such a strategy.

The Mechanics of After-Tax Contributions and “Backdoor” Roth Conversions

The Mega Backdoor Roth 401(k) strategy operates through two sequential steps permitted under IRS guidelines. First, participants make contributions to the after-tax sleeve of their 401(k) plan, after maxing out their standard pre-tax or Roth 401(k) contributions. Second, these after-tax 401(k) funds are then immediately converted to the Roth 401(k) or Roth IRA through either:

- IN-PLAN ROTH CONVERSIONS - direct transfers within the 401(k) (ideal scenario)

- IN-SERVICE DISTRIBUTIONS - rollovers to a Roth IRA while still employed (complex scenario)

In 2025, the total combined contribution limit for 401(k) plans—including employee deferrals, employer matches, and after-tax contributions—is $70,000 ($76,500 for those aged 50+). It is this “after-tax contribution” that allows us to fund the Roth 401(k) sleeve via the “backdoor” conversion.

AN EXAMPLE: A 45-year-old earning $300,000 who contributes $23,500 to a pre-tax 401(k) and receives a $10,000 employer match could potentially contribute an additional $36,500 via the backdoor 401(k) Roth strategy. ($70,000 total IRS limit - $23,500 employee - $10,000 employer match = $36,500 remaining to contribute).

If implemented correctly, this strategy can be executed without creating any additional tax impact on your return. This individual makes too much to contribute to a Roth IRA, and even if they could, these contributions are capped at $7k/year. Thus, this strategy earned the name “Mega Backdoor 401(k) Roth Conversion.”

Personal Financial Prerequisites:

To benefit from this strategy, individuals must:

- Maximize standard 401(k) employee contributions: $23,500 in 2025 ($30,500 for ages 50+).

- Have sufficient cash flow to allocate additional retirement savings beyond standard limits. Again, this strategy should only be implemented as part of a holistic financial planning process.

Employer Plan Requirements: Not all 401(k) plans support this strategy. Participants must verify their plan allows:

- After-tax 401(k) contributions (distinct from Roth 401(k) contributions)

- In-plan Roth conversions or in-service distributions: Only ~11% of 401(k) plans permitted Mega Backdoor Roth conversions in 2023.

401K PLANS WITH THE IN-PLAN ROTH CONVERSION MECHANISM IN PLACE: Microsoft, Amazon, Google, Alphabet, Meta, Expedia, Oracle, Salesforce, Dell, IBM, VMware, Cisco, Nvidia, Intuit, Atlassian, and many other large corporations.

Strategy Implementation Steps

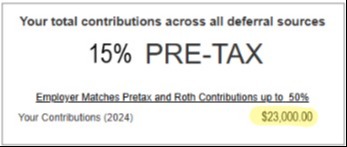

STEP 1: Maximize your standard pre-tax or Roth 401(k) contributions for the year.

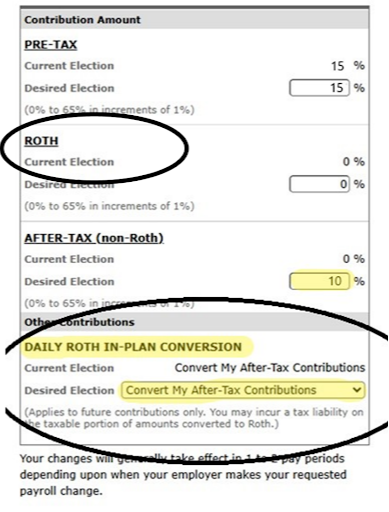

STEP 2: Once you’ve reached the regular annual limit, update your 401(k) saving elections to contribute to the “After-tax (non-Roth)” section of your 401(k).

STEP 3: Ensure the “DAILY ROTH-IN PLAN CONVERSION” is set to “CONVERT MY AFTER-TAX CONTRIBUTIONS”.

NOTE: If your 401(k) doesn’t have this Daily Roth-In Plan Conversion option online, there is likely an 800-number you can call to implement this quickly. For example, Expedia requires employees to call in to implement this strategy. You only need to call once; however, you do not need to call for each conversion.

DONE: You will now have assets in the Roth section of your 401(k), with no additional impact on your income tax status. These Roth assets grow tax-free and retirement distributions will also be tax-free.

IMPORTANT NOTE: This strategy does require funds to stay in the retirement account until age 59½ or penalties may be assessed on distributions. For this reason, it may not be appropriate to maximize retirement savings if cash is needed for purposes other than retirement.

You can reach out to me at any time at ktemple@mirusplanning.com to learn how we at Mirus Planning help our clients implement these strategies.